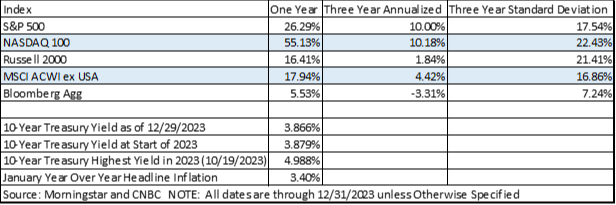

2023 started with a whimper and ended with a bang, with markets trading sideways in the beginning but steadily improving as interest rates normalized by the end of the year. All the major indices ended the year higher than where they started, with the equity benchmark S&P 500 up 26.29%, the tech heavy NASDAQ 100 up an eye-popping 55.13%, the small-cap Russell 2000 up 16.41%, the international MSCI ACWI ex USA up 17.94%, and the fixed income benchmark Bloomberg Agg up 5.53% for the year. These large increases across the indices were aided by an end of year rally, with the S&P 500 jumping 11.14% in the fourth quarter alone. Given this progress, both the NASDAQ 100 and the S&P 500 have broken through their previous all-time highs from December of 2021. While it is exciting to see new highs, it is important to put this new level in context. The return on the S&P 500 from 12/31/2021-12/31/2023 was .07%, meaning that for the past two years, performance has been essentially flat.

As seen in the chart below from J.P. Morgan, the solid performance in 2023 across all asset classes (with the notable exception of commodities), has led to a recovery from the large losses seen in 2022. A key driver of this recovery has been the normalization of interest rates, which in turn was precipitated by the taming of inflation. While still above the Fed’s target of 2%, January’s year-over-year inflation print of 3.4% is considerably lower than previous numbers. The positive performance of the markets certainly has been welcome news, especially considering the dismal performance across almost all asset classes in 2022. When just looking at the numbers, 2023 appears to be an excellent year. However, it is important to remember that while the year recorded solid returns, there were several periods in 2023 where it was not apparent that this would be the case. In this newsletter, we will review the major events of 2023 as well as the areas we are looking at as we begin 2024.

The first major test of the markets came in March of 2023, with the collapse of Silicon Valley Bank, Signature Bank, and First Republic Bank, precipitating a regional banking crisis as depositors worried if their local banks were vulnerable as well. Taken together, these three banks held more than $500 billion in assets – a staggering sum that, adjusted for inflation, exceeds the holdings of the twenty-five banks that collapsed during the global financial crisis of 2008, per the BBC. Experts contend that the reasons for these bank collapses were due to heavy exposure to low-yielding loans that decreased in value as interest rates rose, combined with the ease of moving funds out of the banks, exacerbating a classic bank run as depositors worried about the value of the assets backing their accounts.

In May, the markets reacted positively to the mainstreaming of artificial intelligence (AI), with programs like Chat GPT and Google’s Bard gaining more widespread adoption. A chief beneficiary of the AI frenzy was American computer chip manufacturer Nvidia, which produces approximately three-fourths of all the chips used to power AI applications. By the end of May, Nvidia topped a trillion dollars in market capitalization, joining this select club alongside Apple, Microsoft, Alphabet and Amazon. The need for advanced chips to power AI breathed new life into the previously stale computer chip manufacturing sector, greatly benefiting Nvidia but also its competitors, who are attempting to claim market share in this space. While Nvidia is certainly the big winner of 2023 (gaining 238.9% for the year), it is joined by other tech companies in the so-called Magnificent Seven companies, with their gains substantially higher than the S&P 500’s 24.2% return in 2023. Besides Nvidia, the other Magnificent Seven firms are Apple (up 48.2% for 2023), Microsoft (up 56.8%), Alphabet (58.3%), Amazon (up 80.9%), Meta (up 194.1%), and Tesla (up 101.7%).

Besides Nvidia, the other Magnificent Seven firms are Apple (up 48.2% for 2023), Microsoft (up 56.8%), Alphabet (58.3%), Amazon (up 80.9%), Meta (up 194.1%), and Tesla (up 101.7%).

October saw two troubling events for the markets, one tragic and the other concerning. First, on October 7th, Hamas terrorists stormed into southern Israel, killing over one thousand people and taking 247 people captive, some of whom are still held hostage to this day. This terrifying incursion was the first invasion of Israeli territory since the 1948 Arab-Israeli War. While the loss of life is tragic, its effects on the markets have been somewhat muted. On the crypto front, October saw the trial of Sam Bankman-Fried, the former head of disgraced and bankrupt crypto brokerage firm FTX. The fallout from this trial exposed the risks associated with the crypto industry and was a major wakeup call for investors on the importance of due diligence when selecting a crypto currency brokerage.

2023 ended on strong footing with the S&P 500 gaining 4.5% for December alone, in what could be called a “Santa Claus” rally. While these solid returns set up investors in a strong position going into 2024, there is much uncertainty in the world that could lead to heightened volatility in 2024. Here are several items that are on our radar:

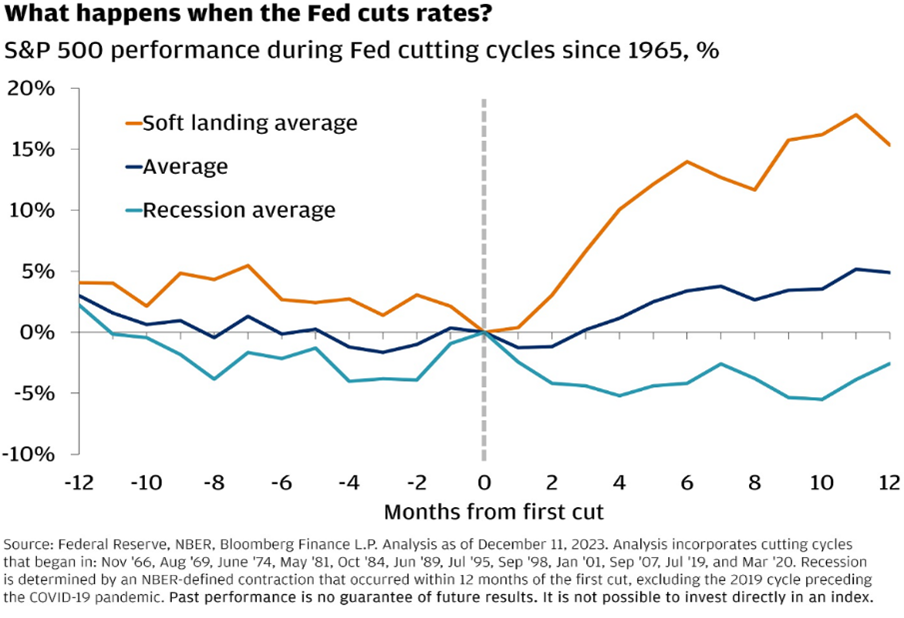

- Where will interest rates go? Most economists are expecting interest rate cuts in 2024, assuming inflation remains under control. The Fed’s own FOMC is projecting benchmark rates to drop to 4.5% by the end of the year, down from the current 5.25%-5.50% band. This could be very good news for investors. Per J.P. Morgan, the S&P 500 typically rallies by roughly 15% on average in the 12 months after the first Fed rate cut (based off data going back to 1965). This chart paints a rosy picture should interest rates go down in 2024.

- 2024 is an election year in the U.S. Historically, this has meant more volatility in the markets as there is uncertainty about which party will end up with control of Congress and the White House. While there is certainly volatility in the runup to the election, this tends to be very short-term and does not impact the year’s overall performance. Since 1896, there have only been 6 election years when the market has dropped by more than 5%, per the 2024 Stock Trader’s Almanac.

- As mentioned above, the conflict between Israel and Gaza has not materially impacted markets. However, with Iran-backed Houthi rebels in Yemen harassing container ships in the Red Sea as retaliation against Israel, global shipping could be seriously impacted. With 30% of world container traffic and 12% of the seaborne oil trade ordinarily passing through it, any disruption to the peaceful flow of trade through the Red Sea could have a serious impact on the global economy. Major firms are already avoiding the Suez Canal and the Red Sea as a safety precaution. If this is to continue and the shippers pass on the added expense to consumers, prices could rise as cargo take longer routes to avoid this area.

In conclusion, while we do not know how 2024 will turn out, it is safe to say that it could be a year of heightened volatility due to domestic politics and international events. While it is normal to be concerned about volatility, the best defense against it, is to stick to your long-term investment plan. We look forward to continuing to work with you in 2024 to adapt to and embrace the opportunities brought forward by the evolving markets.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Compton Wealth Advisory Group, LLC ["Compton]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Compton. Please remember to contact Compton, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Compton is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of Compton’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at http://www.comptonwealth.com. Please Note: If you are a Compton client, Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Compton account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Compton accounts; and (3) a description of each comparative benchmark/index is available upon request.

Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if Compton is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation data/criteria, to the extent applicable). Unless expressly indicated to the contrary, Compton did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of Compton by any of its clients. ANY QUESTIONS: Compton's Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.