2025 is now in the books. This frenetic market started out optimistic, pivoted to despair over trade turmoil, and then finished the year strong despite geopolitical uncertainties. In this newsletter, we will recap the three major phases of the market over last year and show where that leaves us as we start 2026.

Investment Returns (as of 12/31/2025)

Part 1: A Cautiously Optimistic Start

The market started the year strong for both equities and fixed income, respectively exemplified by the S&P 500 rising 2.78% and the Bloomberg Agg rising .53% in January. Value stocks finally outperformed growth stocks, while bonds eked out a decent return on the back of favorable inflation reports. The US market seemed comforted by the peaceful transfer of power between presidential administrations and hopeful that business conditions would remain favorable. Value stocks looked poised to finally get some time to shine in the spotlight and lead the equity market higher, while bonds still offered attractive, stable yields. January and February were relatively quiet and suggested that maybe 2025 would be less volatile than years passed.

Part 2: He Wasn’t Bluffing

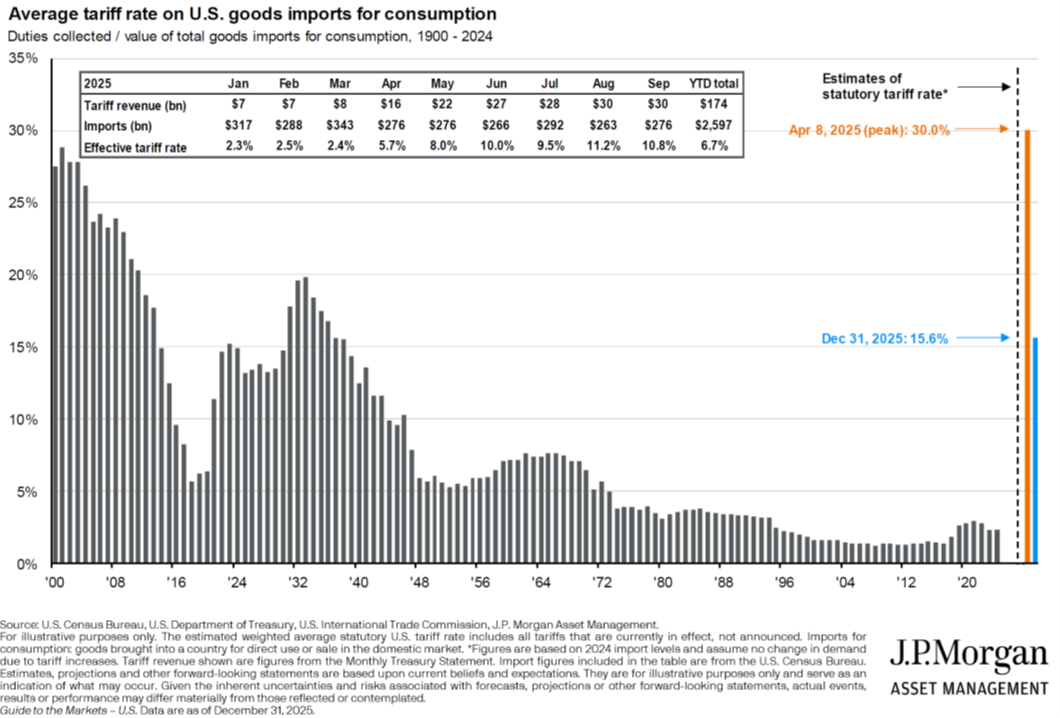

On April 2nd, President Trump announced his massive tariff regime and declared it to be “Liberation Day”. The stock market reacted negatively, with the S&P 500 dropping 5% and the tech-heavy NASDAQ dropping 6% on that day. Equity markets continued to decline the week following as companies and countries scrambled to respond to the new tariffs. The S&P 500 was close to 20% off its February high by April 8th. On April 9th, President Trump announced a pause in tariff implementation and a reduction in some of the most extreme tariffs. Since then, with only minor interruptions, the stock market has moved steadily higher. Below is a chart from J.P. Morgan that shows the recent tariff changes and puts them in the broader historical context, going back to 1900.

Concurrent with the tariff announcements, Congress was working on the Republican’s tax plan. This eventually passed and was signed into law on July 4th. This package made immediate depreciation of tangible asset investments and research and development costs permanent, made the tax cuts found in the expiring Tax Cuts and Jobs Act of 2018 lasting, and doubled the gift and estate tax exemption.

Part 3: Finishing Strong but Feeling Uncertain

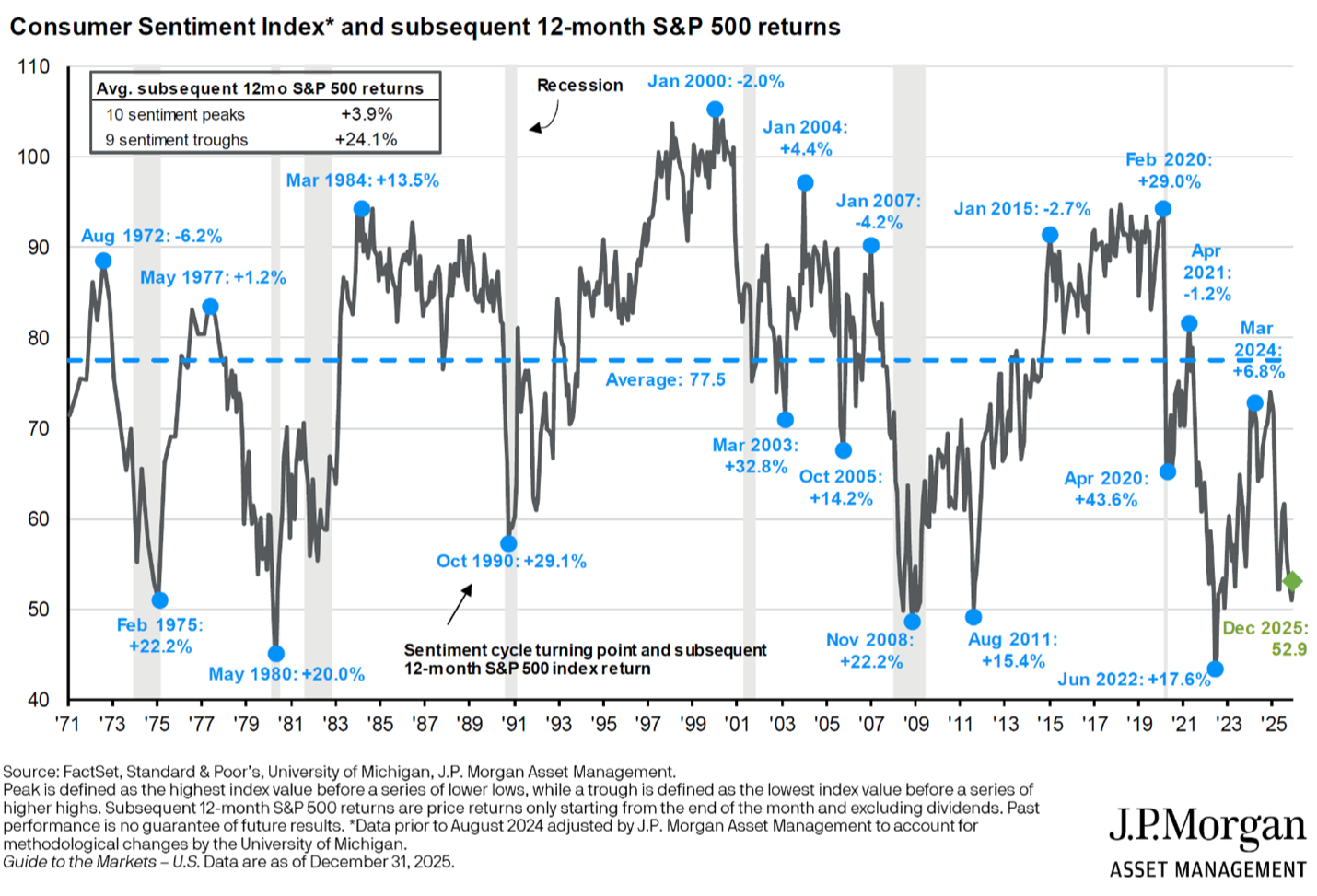

Fast forward to the end of the year and all the major indices secured above-average returns. Stocks and bonds, whether domestic or foreign, had a banner year in 2025. The big winner was international stocks, which finally outperformed domestic stocks after years of lagging far behind. The AI narrative continues to hold as we see companies implement it in their operations. Despite these large gains, a relatively healthy jobs market, and an ongoing Fed easing cycle, the average American does not feel good about the economy. The December University of Michigan Consumer Sentiment index hit 52.9 in, which is just slightly above its all-time low of 50 from 2022 during the COVID inflation peak. Inflation is still above target, and geopolitical uncertainty abounds, with the most recent example of this being the US’s apprehension and extradition of the indicted strongman leader of Venezuela, Nicholas Maduro, on January 3rd.

Concern is a natural human emotion, especially when it involves your hard-earned wealth. In an unsettling world where the markets perform well but the economy feels anxious, it is important to take a step back and focus on what you can control. Your core goals have not changed and we plan for volatility. Rebalancing, cash management, diversification- these tools and others at our disposal are most important at times like these. There is a silver lining to this uncertainty as well. As you can see from the chart below, consumer sentiment and stock market returns often travel in opposite directions. Often, when the masses are most concerned about the economy, that is when solid opportunities present themselves. Staying on the course with your long-term plan allows the patient investor to capitalize on those opportunities.

As we look ahead to 2026, uncertainty remains but there are reasons for optimism. GDP growth in the United States increased at the end of 2025 and could continue around 4% or better if infrastructure investment continues to rise. The rate of change in inflation could also decrease due to multiple factors including no further increases in tariffs and productivity improvements from technological advances, including artificial intelligence. An environment with rising GDP growth and a steady or decreasing rate of inflation has historically been a favorable environment for the stock market. That type of environment may lead to a broadening positive performance beyond the Magnificent 7 stocks into value stocks and smaller company stocks. Additionally, both political parties are motivated to offer financially favorable policies before the midterm elections, driving parts of the economy and markets higher. Geopolitical risks are high and unexpected events could transpire at any time, leading to market volatility. Thus, we will maintain diversification in portfolios and work with all our clients on their specific situations to be sure they have conservative investments for their near-term cash needs.

IMPORTANT DISCLOSURE INFORMATION

Compton Wealth Advisory Group, LLC (“Compton Wealth”) is an SEC registered investment adviser in Virginia Beach, VA and not affiliated with your bank or brokerage custodian. Registration of an investment advisor does not imply any level of skill or training. The information presented is limited to general information pertaining to Compton Wealth’s services, views, outlooks, and opinions and is for information purposes only. There is no guarantee that the views and opinions expressed in any Compton Wealth content will come to pass. The information presented is subject to change without notice and should not be considered an offer to sell or a solicitation of an offer to buy any security.

Certain information presented may contain a discussion of material economic conditions and/or events that may affect future results. All information is deemed reliable as of the date presented but is not guaranteed and is subject to change.

Certain information is based on or derived from independent third-party sources that, in certain cases, may or may not have been updated through the date of this information. While such information is believed to be reliable for the purposes used herein, Compton Wealth has not independently verified the assumptions on which such information is based nor assumes any responsibility for the accuracy or completeness of such information. Such information is subject to change without notice to you.

References to indices or other financial benchmarks are provided for illustration purposes only. Indices are unmanaged, statistical composites and an individual cannot directly invest in an index. Any returns portrayed do not reflect the deduction of underlying investment expenses and third-party fees to purchase the securities they represent. Data from the indices (i.e., the S&P 500) are supplied by third party suppliers. Compton Wealth does not attest to the accuracy or reliability of these numbers nor the methods of calculation from which they are derived. The indices performance data reported represents past performance and does not guarantee future results. Your current account performance may be lower or higher than return data quoted within.

Past performance does not guarantee future results. Certain information set forth herein may contain “forward-looking information”. These statements are not guarantees of future performance and undue reliance should not be placed on them. Different types of investments involve varying degrees of risk. Therefore, there can be no assurance that the future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Compton Wealth, or any non-investment related content), will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Compton Wealth is neither a law firm, nor a certified public accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this presentation serves as the receipt of, or as a substitute for, personalized investment advice from Compton Wealth. Please remember that it remains your responsibility to advise Compton Wealth, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request at www.comptonwealth.com/disclosures. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Compton Wealth account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Compton Wealth accounts; and (3) a description of each comparative benchmark/index is available upon request.