Markets in Motion 2025: Special Newsletter

2025 has turned out to be highly volatile for markets so far. It is challenging to keep up with all the news coming out of Washington. However, the recent tariff announcements have had a greater impact than many other events. The new tariffs mark the sign of a regime change that has rattled markets and caused extreme volatility. We remain focused on our clients’ long-term goals while paying attention to near-term risks and opportunities. Below are some of the items we are focusing on during this historical period.

Tariffs

The tariffs announced on April 2nd took effect on April 9th, but later that afternoon, the White House announced a 90 day pause for reciprocal tariffs on all countries except China, to allow time for negotiations. Uncertainty remains, but at a reduced level.

1. How long will the tariffs be in place and are there more tariffs to come?

2. With a new 90 day negotiating window, what deals will the United States make with certain countries, and what are the long-term impacts?

3. Will China go into a protracted trade war with the United States that forces companies to adjust their supply chains and working capital needs?

Risks to the Markets

There are always risks in investing, but the tariffs and current growth slowdown are highlighting a few specific risks.

1. CEOs are likely to cut back on their capital expenditures. If tariffs seem likely to remain for the long term, layoffs could increase.

2. Companies may not be able to pass along higher prices to consumers despite having higher costs of goods sold from their suppliers.

3. Concerns about market volatility along with fears of layoffs may lead consumers to reduce spending, thus causing a downward loop of even lower stock prices and increased layoffs.

4. Credit – there is a significant amount of debt coming due for both the federal and state governments as well as US companies in the next two years. Refinancing that debt is harder if there is a stagflationary environment where growth slows but inflation and interest rates remain high.

5. Recession – The risk of recession was reduced after the pause in tariffs announced on April 9th, but an elevated risk remains. If a recession occurs, there is a greater chance of a technical recession like in 2022 (two quarters of negative GDP growth) rather than an official recession declared by the National Bureau of Economic Research; NBER, (where unemployment is higher and economic conditions deteriorate significantly). Historically, technical recessions have not had as much stock market downside as official recessions declared by NBER. Below is a chart from Liz Ann Sonders at Charles Schwab that succinctly lays out the interplay between bear markets, their duration, and recessions. As seen below, it is interesting to note that one does not necessitate the other.

Upside Opportunities for Markets

There are a wide range of outcomes for markets in the near term and we see the potential for various events with the potential to drive stock market prices higher.

1. Reductions in Tariffs – as evidenced by the White House announcement on the afternoon of April 9th, the stock market can move higher rapidly if trade uncertainty is reduced in favor of lower tariffs or the potential for trade deals.

2. Tax Legislation – Congress is currently working through negotiations on legislation to extend tax rates from the Tax Cuts and Jobs Act. The White House would like to enact additional tax provisions proposed by President Trump on the campaign trail. Achieving this is likely to be positive for the stock market.

3. Federal Reserve easing – The Federal Reserve can add liquidity to markets by going back to a policy of quantitative easing. They have already reduced their quantitative tightening policy in 2025 and a switch to quantitative easing at some point is likely to increase stock prices at the index level.

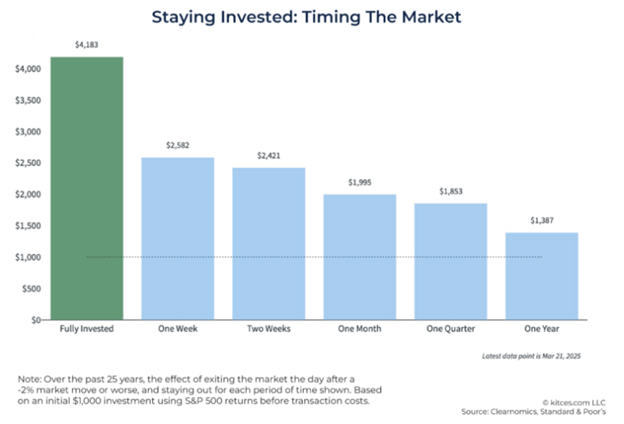

These market moves can be scary. However, it is important to recognize that the selection and management of investable assets are tools within a financial plan. Based on your goals, a financial plan will guide you in allocating your assets in a way that is appropriate for your risk tolerance and timeline. Modifications to your investment allocations should only be driven by a change in your own unique financial circumstances and not market movement. Reacting emotionally to a downturn by reducing market exposure tends to result in worse performance. As seen in the chart below from Kitces, selling out of the market and staying out for just a week, nearly halved investment returns over a 25-year period; waiting a year led to a nearly four-fold decrease in returns.

We remain committed to managing your portfolio with the goal of making sure that your financial strategies align with what matters most to you. As always, please let us know if we can answer any questions about current market conditions, or your personal investment portfolio. We are available at 757-351-0741 or we can set up a time to meet.

Important Disclosure Information

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Compton Wealth Advisory Group, LLC [“Compton Wealth]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Compton Wealth. Compton Wealth is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of Compton Wealth’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.comptonwealth.com.

Please Remember: If you are a Compton Wealth client, please contact Compton Wealth, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Compton Wealth account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Compton Wealth accounts; and (3) a description of each comparative benchmark/index is available upon request.

Footnotes:

1

2

Source: Kitces.com LLC. Clearnonomics, Standard & Poor’s.