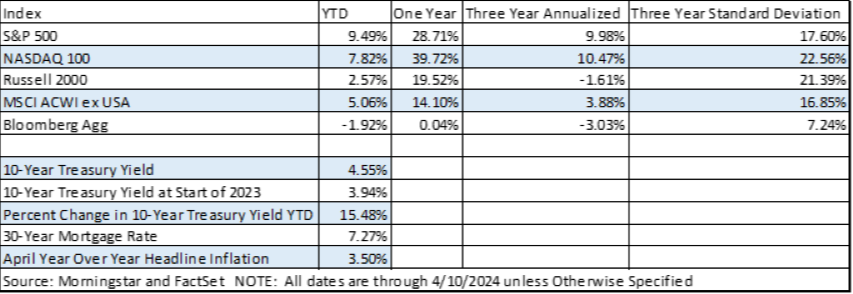

The first quarter of 2024 continued the momentum from the last quarter of 2023, richly rewarding equity investors while providing slightly negative returns for fixed income. The large-cap S&P 500 delivered a strong 9.49% return, surprisingly higher than the 7.82% return of the tech-heavy NASDAQ 100, which until now has led the way for equities. While positive, the Russell 2000 (small cap) and the MSCI ACWI ex USA (international) returns were paltry by comparison, posting 2.57% and 5.06% gains, respectively, suggesting that the market rally is still largely confined to large, U.S. stocks. The Bloomberg Aggregate Bond Index, a proxy for the bond market, returned -1.92%, a consequence of the Fed’s decision to keep rates “higher for longer”. Because of the inverse relationship between bond yields and bond prices, higher interest rates tend to lead to negative fixed income performance.

With equity markets hovering around all-time highs and the promise of Artificial Intelligence (“AI”) beginning to permeate beyond just the tech sector, some investors may be having flashbacks to the late 1990s, when tech valuations reached astronomical heights on the hope of the then nascent internet becoming widely adopted. Back then, the possibility of near limitless productivity gains from integrating real-life business with cyberspace drove a speculative frenzy that crashed when markets realized that the full potential of the internet was years away from being realized. Fast forward to today, it can be tempting to see parallels between the hype surrounding AI and the hype around the internet in the late 1990s. However, it is important to note that there are key differences between now and then, while also acknowledging that the market is in fact richly valued. In this newsletter, we will examine why we believe the similarities between now and the Tech Bubble may be superficial, as well as what we should be on the lookout for during periods of such high valuations.

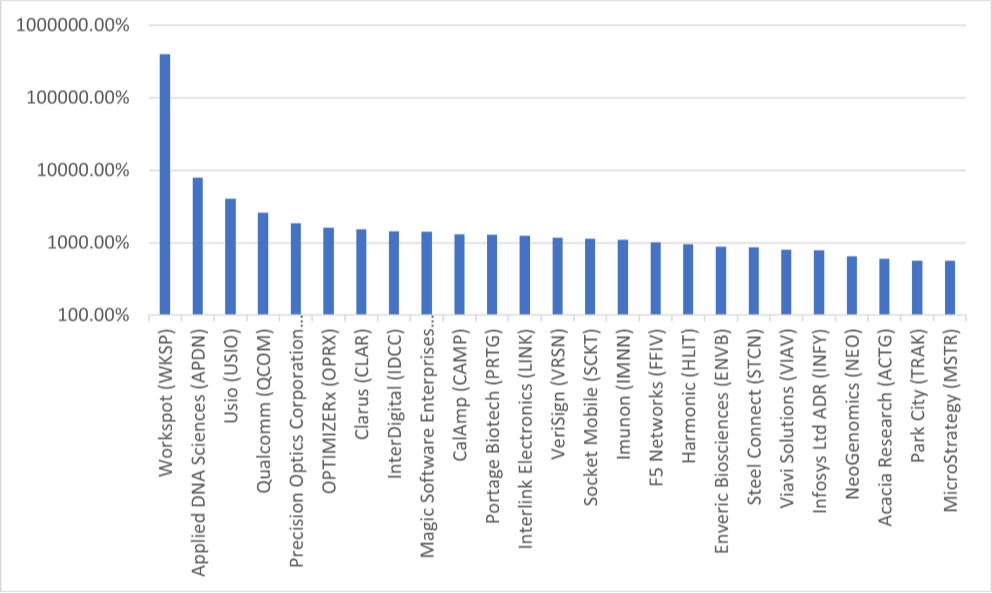

Let’s first put into perspective the current run-up in the stock market by comparing it to 1999. Yes, new technology is driving equities to all-time highs, but when looking at the scale of these price-pops, the comparison between now and the Dot-Com bubble looks deficient. Below is a chart with data from Statmuse showing the jaw-dropping returns of the top-performing stocks of 1999.

The top performing stock back then was the remote computing firm Workspot, which returned an astronomical 399,900.80% in 1999. So massive was this increase that we had to change the Y-axis in the above chart to logarithmic just to show the performance of the other top-performing stocks from that year. By 2005, Workspot was defunct, a fate shared by many of the other firms on this chart. In fact, only a few, like MicroStrategy or Qualcomm, are even recognizable businesses still in operation today. Contrast this with today, where the top performing commonly traded stock of 2023 was Coinbase, with a meagre (by comparison) annual gain of 391.4%, driven largely by the rally in Bitcoin. Nvidia was the second-place finisher, with a 239% increase, a true beneficiary of the AI boom, as it manufactures the chips that power the technology. While equities, particularly tech equities, have had tremendous advances as of late, this pales in comparison to the run-ups seen in 1999.

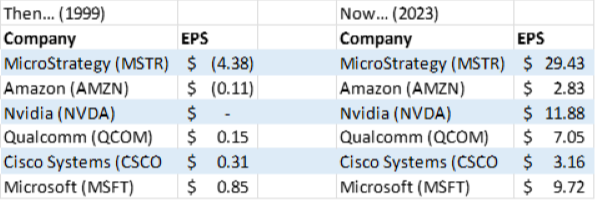

Aside from the magnitude of the run-up in tech stock prices, another key difference between then and now is the critical fact that tech firms today are profitable. We put together a table of well-known tech stocks from 1999 that survived through to today. As you will see below, these stocks had low-to-negative profits as represented by Earnings per Share (EPS) in 1999, while today they have matured into cash-generating behemoths.

This table only considers 6 well-known stocks operating in 1999 that continue to exist today. There were countless examples of high-flying tech stocks in 1999 that were hemorrhaging money (see Pets.com), while today’s tech companies prove to be highly profitable, with the Magnificent 7 (Apple, Microsoft, Alphabet, Amazon, Meta Platforms, NVIDIA, and Tesla) providing 25.5% of the S&P 500’s earnings, per FactSet. This is critical to point out because earnings are what support stock prices. Unlike in 1999, today’s admittedly stretched valuations of many technology companies are at least balanced by strong profits, suggesting less of a speculative frenzy.

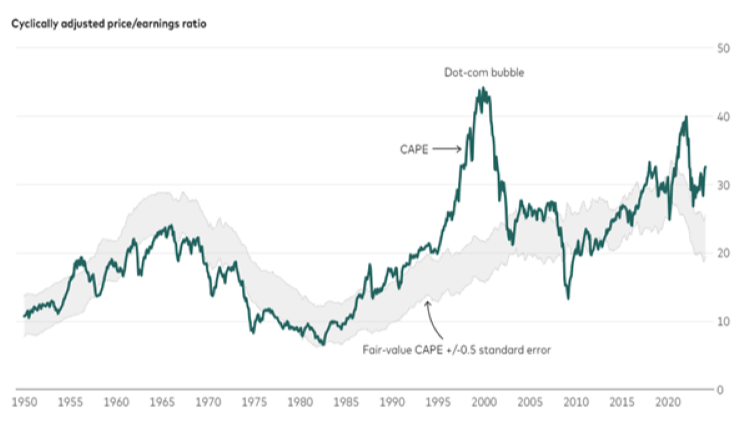

In fact, Vanguard notes that this valuation is at the 99th percentile, a level paralleled since 1950 only by the Dot-Com bubble and the post-COVID reopening.

While it is certainly comforting to know that the highly valued companies of today are at least backed by solid profits, unlike during the Dot-Com bubble, the fact remains that the stock market is trading at a rich multiple. A valuation metric that we like to follow is the cyclically adjusted price/earnings (CAPE) ratio, which considers current share prices in the context of 10-year inflation-adjusted earnings per share. Per Vanguard, the January 2024 CAPE ratio for U.S. equities was over 30, higher than in most periods of the last 70 years. In fact, Vanguard notes that this valuation is at the 99th percentile, a level paralleled since 1950 only by the Dot-Com bubble and the post-COVID reopening. Their chart below visualizes where we are in terms of CAPE valuations.

Valuations are a strong predictor of long-term equity performance, so today’s high values suggest that stock returns may be muted in the future. To trim back these high valuations, some combination of earnings picking up, interest rates falling, or stock prices declining must occur. While we hope for the first two options, any seasoned equity investor can tell you that a decline in stock prices is inevitable. Since it is near impossible to predict a market top (and very costly if predicted incorrectly), we avoid trading around these valuations and instead control what we can by setting reasonable return expectations and keeping your portfolio diversified.

Don’t be discouraged if stocks perform below how they have been as of late. That is a normal part of the business cycle. Our strategies at Compton Wealth are inherently well diversified both in the equity sleeve (across market-cap and style) and asset class (with equity and fixed income allocations based off risk tolerance). While we do not believe that we are in the middle of a 1999-like tech frenzy, these high equity valuations necessitate the need to follow these points more than ever.

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Compton Wealth Advisory Group, LLC ["Compton]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Compton. Please remember to contact Compton, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Compton is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of Compton’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at http://www.comptonwealth.com. Please Note: If you are a Compton client, Please advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Compton account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Compton accounts; and (3) a description of each comparative benchmark/index is available upon request.

Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if Compton is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation data/criteria, to the extent applicable). Unless expressly indicated to the contrary, Compton did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of Compton by any of its clients. ANY QUESTIONS: Compton's Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.